Table of Content

If your heirs choose to keep the home, they must refinance it into their own names. If they choose to sell the home, they may have up to 12 months to complete the sale. Remember, the FHA insures the reverse mortgage, so if the loan consumes all the equiy and the home is no longer worth what is owed, the insurance makes up the difference – not you or your heirs. One thing to keep in mind after one year is that you may be able to redo the reverse mortgage. There has to be some sort of tangible benefit, otherwise FHA won’t allow it to happen. For example, sometimes home values increase enough to make it beneficial to refinance a reverse mortgage.

The home must be placed on its original site and left there. There is a Home Equity Conversion Mortgage for Purchase loan that allows people 62 and older to purchase a new principal residence with HECM loan proceeds. This can depend on where you live and the property itself. The appraisal will start at about $500 and can go up if the property is not similar to other properties in the area .

You Can’t Afford The Costs

It makes sense, all of these are built in a centralized location and shipped to their owner’s final destination. So, it makes good sense to quickly differentiate between these home types. According to HUD regulations, it is illegal to remove HUD tags or HUD data plates. Without these, the home will not be eligible for a reverse mortgage. You’ll also need to pay an initial mortgage insurance premium that is 2% of your home’s value in addition to an annual mortgage insurance premium that is 0.5% of the loan amount. You’ll need to work with an HUD-approved lender in order to qualify for the HECM reverse mortgage.

However, some things cannot be ascertained without inspections from engineers and appraisers. But if you get past the first hurdles, at least you know you would not be spending your money on the appraisal and other inspections needlessly by taking your time and checking into the obvious issues first. This article is just the bare basics of getting a reverse mortgage on a manufactured home, but it is a start. Your home must have permanently installed utilities that have been protected from freezing.

What Documents Are Required To Get A Reverse Mortgage And Where Do I Find Them

Your home must be taxed and classified as real estate and must be designed to be used as a dwelling with a permanent foundation built to FHA requirements. The only move the house had to meet was to move from the factory to the seller and then to the site. Being on the site, she had to stay there permanently.

Chances are very good you'll need appropriate skirting too, and the folks who do the foundation will also be able to install the skirting. There are not many lenders who will be ready offer you a reverse mortgage on a mobile home. However you can speak to the lenders and check if they are ready to give you the reverse mortgage. You can even speak to the lenders of this community and seek a no-obligation free mortgage consultation from them. To have a reverse mortgage on a property, it must be your principal residence, meaning that you live there for most of the year. Your reverse mortgage will mature if you're away from the property for more than six months for a nonmedical reason or more than 12 consecutive months in a medical facility.

Should I Refinance My Mortgage To Pay Off Debt

There would be no way to enforce the terms of any loan if the lender could not call the loan due and payable in the event of a default, and there would be no way to enforce such an action on just half the property. Manufactured homes do have specific requirements to meet HUD eligibility criteria but are allowed if they meet the HUD parameters. HUD has very specific guidelines for Manufactured homes and there are very few lenders who will still do them, but they can be done. The structure must be built and remain on a permanent chassis, and it must be connected to the foundation through welds, bolts, and various light gage metal plates.

If they do satisfy the HUD guidelines, then they can be used. To further meet the requirements for a reverse mortgage, the owner must receive an engineer’s certificate claiming that the infrastructure complies with the Permanent Foundation Guide for Manufactured Homes . The borrower is responsible for the costs of obtaining this certificate. The very first items an appraiser will look for are the HUD tags .

QUESTIONS?

You can use the money you get from a reverse mortgage to do this. A manufactured homeowner must meet a dizzying list of requirements and inspections to qualify for a reverse mortgage. If there are not adequate recent sales to indicate the acceptability of the homes in your area, HUD has no way to gauge whether or not the property is readily marketable. This requirement is not exclusive to manufactured homes, HUD requires appraisers to compare homes with similar properties in all instances. The issue we find that tends to cause a problem though is that in rural areas many appraisers have a very difficult time finding at least 3 recent sales of manufactured home properties. You may want to check your area to see what the sales are like as it could very well determine your ability to obtain the mortgage if that is important to you.

The reason I say this is, he will have to put a good amount of money to close on a reverse mortgage. A home equity loan, in my opinion, would be a better option in this situation. If you don't know if you have a permanent foundation, see if form 433A has been recorded against your Title.

With a mortgage balance of $192K, your home will need to appraise for about $390K to move forward with a reverse mortgage with no cash out of pocket. Based on everything you have provided so far, yes, you are eligible for a reverse mortgage. The addition will need to be permitted and built to local code. There will need to be sales of similar manufactured homes in your area in the past year.

To be eligible, the park needs to be fee simple or a condominium park that is on the FHA-approved list. Parks where you lease the land are not eligible for a reverse mortgage. As part of the loan process, an appraisal of the land and home are done. The appraisal will include at least three comparable sales in the past year and a couple of active listings. That sets a precedent for what someone was willing to pay “recently” for a similar offering.

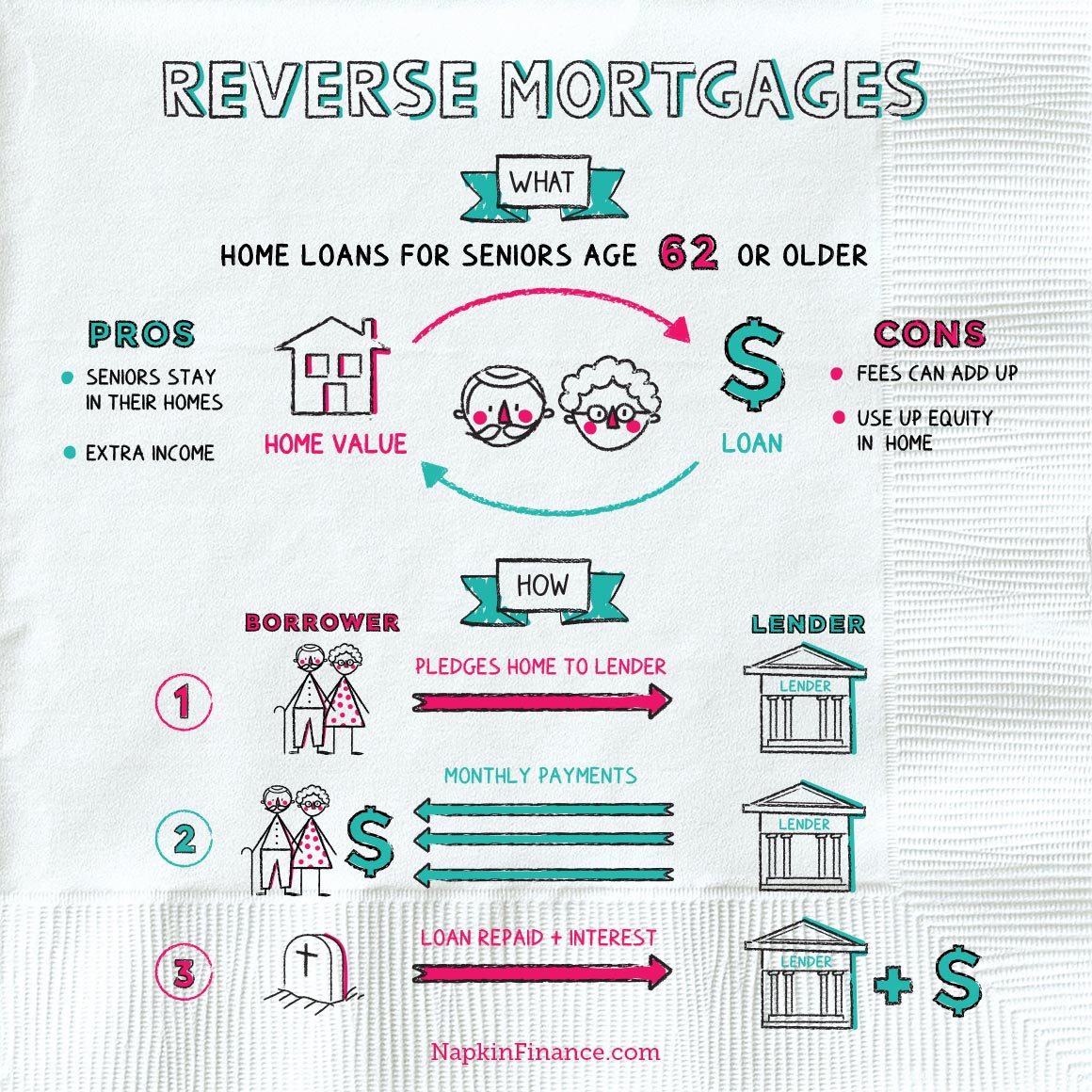

The amount of money you can borrow depends on your age, the value of your home, and current interest rates. You can receive the money in one lump sum, monthly payments, or a line of credit. A reverse mortgage is a loan that allows homeowners to borrow against the equity they’ve built in their home. With a reverse mortgage, you can continue living in your home without making monthly payments.

I would strongly suggest you talk to local real estate professionals to determine what the ramifications of any changes would be before doing anything that would lower your overall value. Before you consider changing the size/dimensions of your lot, you want to be sure that it will not adversely affect your value. The bank will start the foreclosure sale at the amount owed and if no one bids any higher, then the bank would own the property due to no competing bids. With that much equity, there would most likely be other bids at the sale and then the home would go to the highest bidder. If the home has not yet gone through foreclosure, the bank can't sell it - they don't own it.

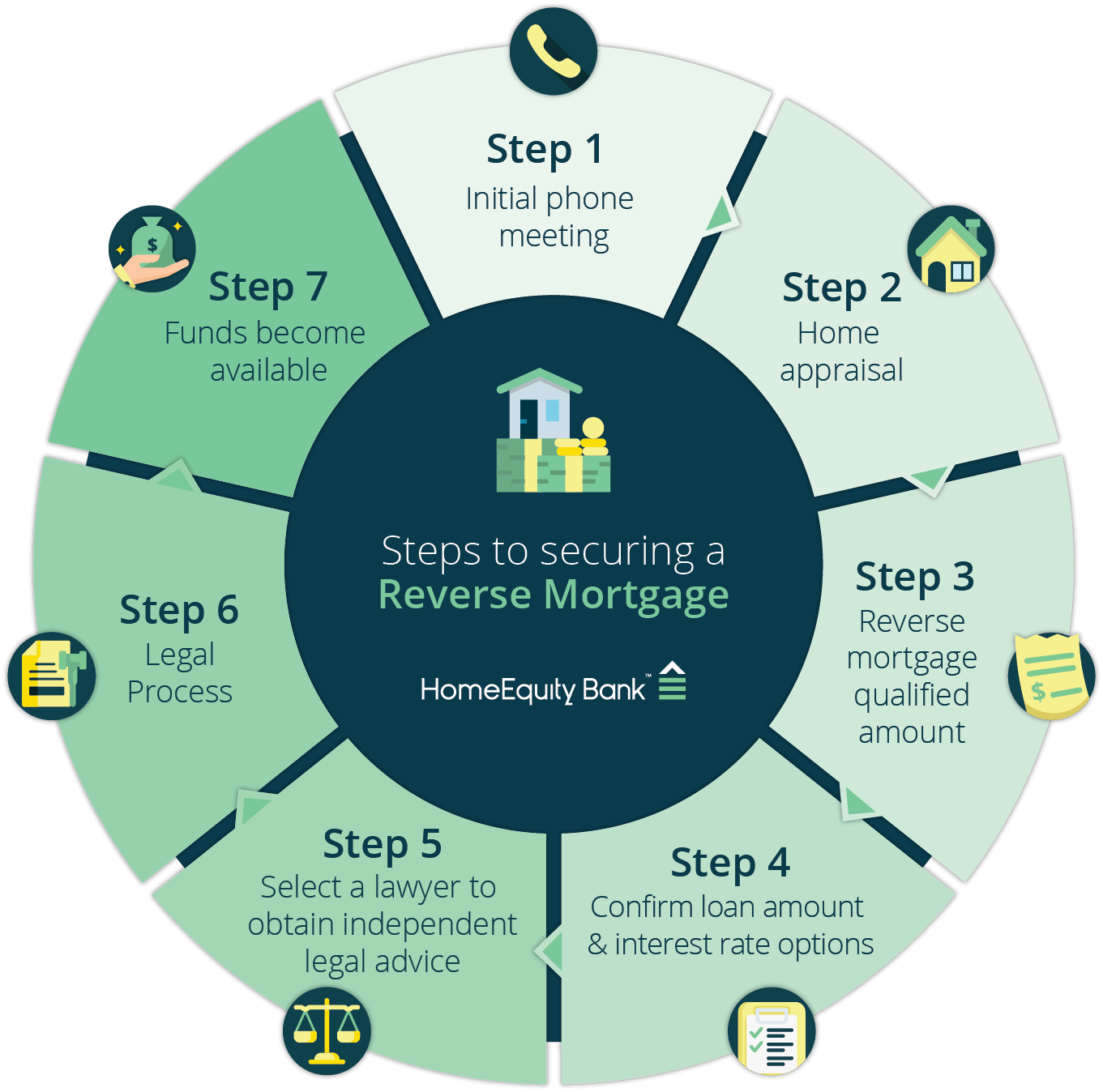

It can typically be found glued to the inside of a kitchen cabinet or bedroom door. Sign all required paperwork and undergo counseling. You can apply for a maximum loan limit of $970,800, which is a significant increase over the previous year. This website has not been reviewed, approved or issued by HUD, FHA or any government agency. The interest of adjustable-rate mortgages are tied to the index and margin.

Typically, any homes that HUD looks at to insure the loans must be readily marketable and that means that there must be recent sales of similar properties for the appraiser to use when determining the value. If there are adequate recent sales of other manufactured homes and the home meets HUD's other requirements, then you can get a reverse mortgage on the property. It’s nothing crazy, but they want you to meet with someone that knows about reverse mortgages, but are not trying to sell you on it. The counselor just goes over the facts (like how you’ll still own the mobile home, how it has to be primary residence, how you need to pay taxes/insurance, etc.). Before applying for a reverse mortgage on manufactured home, prospective borrowers should triple-check that their home meets the extensive list of qualifications defined by HUD/FHA guidelines. After determining eligibility, borrowers should weigh the potential costs and benefits they will incur in the process to ensure that the overall gain is worth the reparations.

No comments:

Post a Comment